Taxation in Taiwan

Taxes provide an important source of revenue for various levels of the Government of the Republic of China. The tax revenue of Taiwan in 2015 amounted NT$2.1 trillion.[1]

Tax administration

The Ministry of Finance, which is part of the Executive Yuan, is the highest government entity responsible for implementing taxation policies and overseeing the leveling and collection of taxes. Taxation occurs at both the national and local government level.

National taxes

Two broad categories of taxes exist at the national level: customs duties and inland taxes. Customs duties are administered by the Directorate-General of Customs, which has local offices throughout the country. Five national tax administrations who are directly subordinate to the central government handle oversight of all inland taxes. Inland taxes is a broad term that includes:[2]

- Income Tax;

- Estate and Gift Tax;

- Value-Added and Non-Value-Added Business Tax;

- Tobacco and Alcohol Tax;

- Commodity Tax;

- Securities Transaction Tax; and

- Futures Transaction Tax

Local taxes

Individual municipalities, counties, and cities have set up Revenue Service Offices responsible for collecting a range of taxes, including:[2][3]

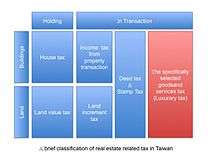

- Agricultural Land Tax

- Land Value Tax

- Land Value Increment Tax

- House Tax

- Vehicle License Tax

- Deed Tax

- Stamp Tax

- Amusement Tax

Tax legislation

Unlike the Internal Revenue Code in the United States, there isn't one law that governs taxation in Taiwan. Rather, taxes are governed by a series of laws and regulations each related to a specific type of tax. As the chief legislative body, the Legislative Yuan plays an important role in formulating and revising tax related laws. The Income Tax Act is the primary law that governs individual income and profit-seeking enterprise income taxes.[4]

Individual Income Tax

Both residents and non-residents are assessed individual income tax on Taiwan-sourced income unless an exception is provided in the Income Tax Act and related laws. Individuals are considered residents of Taiwan for tax purposes if they are either domiciled there, or spend more than 183 days or longer in a taxable year.

Income received in exchange for services rendered while physically present in Taiwan is considered to be Republic of China-sourced income regardless of if the payer is a local or offshore person or entity. One major exception to this rule exists for non-residents who are physically present in Taiwan for less than 90 calendar days in a year and who are only paid compensation by offshore entities.[5]

Progressive tax

Taiwan has implemented a progressive tax system for individual income taxes. For the 2011 tax year, the tax rates were as follows:[6]

| Brackets (Unit NT$) | Rate (%) |

|---|---|

| 0 - 500,000 | 5% |

| 500,001 - 1,130,000 | 12% |

| 1,130,001 - 2,260,000 | 20% |

| 2,260,001 - 4,230,000 | 30% |

| 4,230,001 and over | 40% |

Filing of individual income tax

By default, the tax year for all individuals and profit-seeking enterprises follows the calendar year. Income tax returns are due by May 31 of the following year, with no extension of time allowed.[5] Taxpayers, including foreigners, are able to complete and file their tax return electronically through software provided by the local taxing authority.[7]

Profit-Seeking Enterprise Income Tax

All profit-seeking businesses in Taiwan are subject to the Profit-Seeking Enterprise Income Tax. Sole proprietors and partners must file a return. However, their portion of the taxable income is reported on their individual income tax return.[8]

Income tax rate of profit-seeking enterprises

In 2010, the top tax rate was reduced from 25% to 17%, and the threshold below which no tax is owed was raised from NT$50,000 to NT$120,000. Therefore, the current profit-seeking enterprise tax rates are as follows:[8]

| Taxable Income | Tax Rate |

|---|---|

| Below NT$120,000 | 0% |

| Above NT$120,000 | 17% |

The amount of tax payable shall not exceed half of the amount of the taxable income in excess of NT$120,000.

Securities transaction tax

This tax is paid by sellers of Republic of China securities at a rate of 0.3% of the gross proceeds from the sale of shares issued by companies. A rate of 0.1% applies on the gross proceeds of corporate bonds, however, an exemption has been put in place through 2016.[9] This tax is governed by the regulations set forth in the Securities Transaction Tax Act.[10]

Real estate speculation and the luxury tax

Aimed at cooling off real estate speculation that was driving up the cost of living in Taipei City and other urban areas, the Republic of China government implemented a new luxury tax in June 2011. The law imposes a 15% sales tax on owners of second homes who sell within one year of purchase. Additionally, a 10% sales tax is charged against properties sold after being owned for between one and two years.[11] Data provided by the Republic of China government in late 2011 showed that the luxury tax was having the desired effect, causing the average housing price in Taipei to fall nearly 12% while reducing overall volume of real estate transactions island-wide by nearly 15% in the June–October time period.[12]

Uniform invoice lottery

First conceived in the 1950s, the Taiwan government created a uniform invoice system to encourage honest reporting of sales and prevent underpayment of taxes by businesspeople. To provide an incentive, the government launched a receipt lottery system. Each receipt is coded with an alphanumeric number, and every two months a lottery drawing is held with prizes ranging up to NT$10 million (approximately $335,000 USD as of February 2012) depending on how many numbers match.[13] The lottery is governed by the Uniform Invoice Award Regulations.[14]

Historical tax revenue statistics

| 2010 | 2009 | 2008 | 2007 | 2006 | |

|---|---|---|---|---|---|

| Gross Tax Revenue | 1,565,847 | 1,483,518 | 1,710,617 | 1,685,875 | 1,556,652 |

| Individual Income Tax | 304,686 | 306,804 | 389,744 | 347,526 | 334,330 |

| Profit-Seeking Enterprise Income Tax | 285,701 | 334,163 | 445,245 | 382,634 | 311,888 |

| Unit: NT$ million | |||||

| Source: Guide to ROC Taxes 2011[2] | |||||

See also

Notes and references

- ↑ http://taiwantoday.tw/ct.asp?xItem=241203&ctNode=2182

- 1 2 3 Chapter 1: A General Description of Taxation, Guide to ROC Taxes 2011

- ↑

- ↑ Income Tax Act, Laws & Regulations Database of the Republic of China. Retrieved 24 January 2012.

- 1 2 Introduction to Taiwan tax rules: Taiwan Pocket Tax Book 2011, Page 32. PricewaterhouseCoopers Taiwan. Retrieved 25 January 2012.

- ↑ Chapter 2: Individual Income Tax, Guide to ROC Taxes 2011

- ↑ "Taipei National Tax Administration, Ministry of Finance-e-Filing" Retrieved 25 January 2012.

- 1 2 Chapter 3: Profit-Seeking Enterprise Income Tax, Guide to ROC Taxes 2011

- ↑ Securities Transactions Tax, Taipei National Tax Administration

- ↑ Laws & Regulations Database and The Republic of China. Retrieved 26 January 2012.

- ↑ "Property market seen likely to recover after poll", Focus Taiwan News Channel. Published 15 January 2012. Retrieved 26 January 2012.

- ↑ "Luxury tax is bringing down prices, ministry says", Taipei Times. Published 16 December 2011. Retrieved 26 January 2012.

- ↑ "Unlucky bemoan single digit in invoice lottery" Taipei Times. Published 3 February 2012.

- ↑ Uniform Invoice Award Regulations, Laws & Regulations Database of the Republic of China. Retrieved 2 February 2012.

External links

- Guide to ROC Taxes 2015, Taxation and Tariff Committee

- Taxation Agency

- Taipei National Tax Administration

- Kaohsiung National Tax Administration

- National Tax Administration of Northern Taiwan Province

- National Tax Administration of Central Taiwan Province

- National Tax Administration of Southern Taiwan Province

- Directorate General of Customs

- Local Tax Bureau